A New Retirement Account for Your Kids

By Kawika Shoji

And why it’s worth understanding now.

A few of my parent and grandparent clients have been asking recently about the new “Trump Accounts,” and honestly, I have had the same questions myself. What exactly are these all about? Should I be opening one for each one of my own kids? Good questions. Let’s break down what these accounts actually are (or what the Treasury is telling us they will be), how they compare to the tools you may be already using, and most importantly, where they fit in a plan that actually makes sense for your family.

What are they?

A Trump Account is essentially a starter IRA for a child. Created under the One Big Beautiful Bill Act, these accounts will become available July 4, 2026. The structure is custodial, meaning the assets belong to the child, while a parent or guardian manages the account until the child turns 18. The Treasury has even launched a dedicated app and enrollment site at TrumpAccounts.gov, hopefully making it easy to get started.

Here is the feature generating the most buzz: children born between January 1, 2025 and December 31, 2028 are eligible for a one-time $1,000 federal seed contribution (free money!) to start the account. To claim it, a parent files IRS Form 4547 and registers at TrumpAccounts.gov.

Beyond the seed, up to $5,000 per year can be contributed into the account, and contributors may be parents, grandparents, family, friends, and even employers. Investments are limited to low-cost, broad equity index funds with an expense ratio cap of .10% to prevent the erosion of small deposits. Simple. Clean. Long-term time horizon by design.

There are some constraints and guardrails, however. No withdrawals before the age 18. At that point, the account converts to a traditional IRA, and standard IRA rules apply, including a 10% penalty on early withdrawals before 59 ½.

How it fits in with what you’re already doing?

The Trump Accounts are a useful new tool, but they will work best alongside what you already have, not instead of it. Here’s how I think about the landscape:

529 Plans remain the right tool when college is the primary goal. Contributions grow tax-deferred, withdrawals for qualified education expenses are federal tax-free, and 529s also carry less weight on financial aid calculations than child-owned accounts. Under SECURE 2.0, up to $35,000 in unused 529 funds can eventually roll into the beneficiary’s Roth IRA, a useful safety valve if college costs come in under budget.

UGMA/UTMA custodial accounts offer the broadest flexibility – any goal, any use, no restrictions. The tradeoff is taxes. Investment gains are subject to the “kiddie tax:” the first $1,350 in unearned income is exempt, the next $1,350 is taxed at the child’s rate, and anything over $2,700 is taxed at the parent’s marginal rate. Once the child reaches the age of majority, the money is entirely theirs to do with as they choose.

Custodial Roth IRAs (Roth IRA for Kids!) are quietly one of the most powerful tools available if a child has earned income from a job, self-employment (babysitting!), or paid creative work. Any adult can make the Roth contribution if the earned income is greater than the contribution amount. Contributions can be withdrawn any time without taxes or penalties, and qualified earnings are tax free after 59 ½.

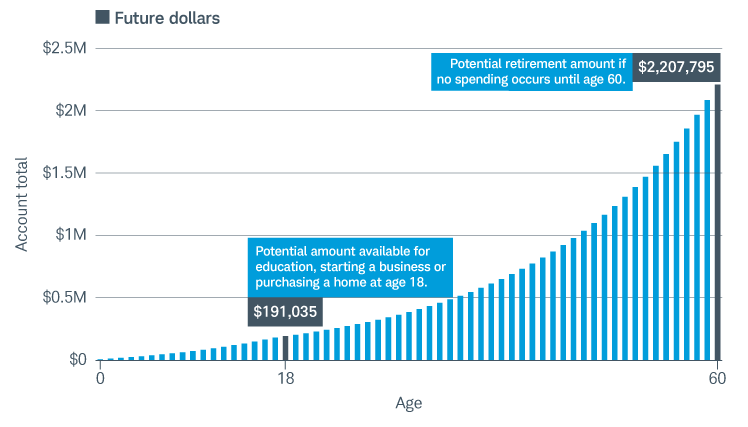

Trump Accounts fill a specific gap: tax deferred growth, no earned income requirement, flexible contributors, and a hard no-touch rule until 18. They’re purpose-built for long-term retirement savings. One nuance worth understanding is that not all contributions are treated the same at withdrawal. Individual contributions from parents and family are made with after-tax dollars, which won’t be taxed again. Employer and government contributions are pre-tax, and will be taxed as ordinary income when the money is withdrawn. All growth in the account, regardless of source, is tax-deferred and taxable upon withdrawal. Traditional IRA rules. Schwab’s analysis suggests a child receiving maximum contribution over 18 years, assuming 6% annualized growth, could accumulate to roughly $191,000 by their 18th birthday, and growing to over $2.2 million by age 60. Time always does the heavy lifting!

Source: schwab.com

What is the money actually for?

Start with a goal. Before choosing a type of account, ask yourself what is this money actually for? If college is the primary goal, then lead with the 529. If your child qualifies for the Trump Account seed contribution, claim it (remember it’s free money!) for their retirement, then continue directing education savings in the 529. If long-term retirement savings is the mission, prioritize the Trump Account. Once your child has earned income, layer in a Roth IRA for kids. If the goal is flexibility for a first car, an early business venture, home downpayment, etc., claim the Trump Account seed, but then also use a UGMA/UTMA account for everything else. You can still add the Roth for kids once earned income begins too!

*A Roth Conversion of the Trump Account may make a lot of sense, but timing will matter. If your child is still a dependent, hold off because the kiddie tax will still apply, and the conversion income gets taxed at your rate, not theirs. Waiting until the child is financially independent to do the conversion will be crucial.

Don’t Overlook the Gifting Piece!

Neil Rose previously wrote in his Grandparent’s Guide to Gifting: “There are few things more satisfying than helping the people you love most get a head start in life. Good news: the tax code is quite generous to grandparents who want to give.” It’s actually quite generous for anyone to give.

Contributions to Trump Accounts are treated as gifts, so at a maximum of $5,000 per year per account, you’ll hit the cap long before the annual gift tax exclusion ($19,000 in 2026) becomes a concern. A parent or grandparent can contribute to a Trump Account and then also to a 529, UGMA/UTMA, or Custodial Roth IRA without triggering gift tax ramifications as long as the total stays under the $19,000. The biggest distinction that 529s offer is superfunding: contributors can front-load up to five years of contributions at once ($95,000 per beneficiary) without touching their lifetime exemption. Thus, in general the 529 still holds the advantage when a grandparent or parent wants to make a large, tax efficient transfer to the next generation, but the Trump Accounts may be better suited for smaller, steady contributions from family members.

Let’s Chat

These accounts are new, guidance is still evolving, and the right approach depends on your family’s goals and tax situation. If you have kids or grandkids and want to discuss some of these options and see if they are right for you, I’d love to connect!

This material is for informational and educational purposes only and does not constitute tax, legal, or investment advice. Tax laws are subject to change, and individual circumstances vary. Please consult your tax and legal professionals for guidance specific to your situation.

About the Author

Kawika Shoji is an investment advisor and portfolio manager at Regency Capital Management. He advises individuals, families, retirement plans, and institutions to assess, develop, and implement their investment and financial goals.