“Big Picture” macro investing often leads to overreacting based on the news of the day. Been there, done that, guilty as charged.

Most often news proves insignificant in the big scheme of things. However, I think new war with Iran is actionable, especially during a time of market froth and general complacency.

At the very least, the war justifies additional conservatism. We are also starting an allocation in the energy sector and a fertilizer giant while further culling investment in technology and consumer stocks.

Strait of Hormuz

Despite war posturing and rhetoric on both sides for years and last year’s bombing of Iran’s main nuclear facility, the war caught the world by surprise.

Trump expected a few days of bombings that would allow the Iran people to finally overthrow the government. Now the whole thing looks like it has the potential to be Trump’s Waterloo.

Markets-wise, the biggest factor is the Strait of Hormuz, the world’s most important oil passage. Just 33 kilometers at its narrowest, the strait traffics 20% of the world’s oil consumption. The vast majority of its 20 million barrels go to Asia. Traffic today is almost none as Iran attacks everything sailing through it.

The Strait has been critical for Japan, Korea, India, and China.

| Country / Region | % of Oil Imports from Strait of Hormuz |

|---|---|

| Japan | 75% |

| South Korea | 60% |

| India | 50% |

| China | 45–50% |

| Europe | 10–20% |

| U.S. | 7–8% |

Europe and the U.S. have easy replacements for supply, especially the U.S. which imports as much as it exports. Bottom line is I think there’s a good chance markets become less complacent about oil and geopolitics. Pricing should adjust accordingly.

Considerations

On the margin, the relative effects are somewhat predictable given regime change in Iran looks unlikely; the state seems too large and pervasive, with a structure of competing military branches making a coup impossible. Regime change may require complete destruction and chaos, which seem unlikely unless the U.S. commits troops on the ground and who knows how much money.

Other considerations we are incorporating include:

- Oil and gas prices should be higher in the next two years than in the last two. Even though the U.S. has decimated much of its defense infrastructure, Iran still has many bases and launch points across hundreds of miles of its coastline. Its ability to send swarms of low-cost drones has proven effective so far. Iran doesn’t need complete control of the strait to prevent tankers full of oil and liquified natural gas (floating bombs themselves) from sailing.

- Markets take time to raise medium term oil price expectations and re-rate stocks according. Oil prices are nearly 50% above where they were a month ago. Over time this means earnings among oil and gas companies, especially American ones, can rise significantly.

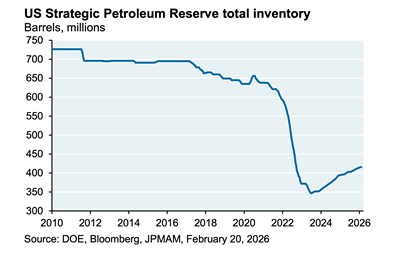

- Yesterday world leaders agreed to release 400 million barrels of state-owned oil with the U.S. providing nearly half. A problem is the U.S.’s strategic petroleum reserves are low after major releases from the Biden Administration. Today, the reserve only covers 20 days of U.S. consumption and will be cut in half after the newest release by the Trump administration. Oil prices haven’t fallen despite the news; markets can do the math. Government reserves are tiny. A good source of strategic oil reserve info can be found here.

- Just a small shift of investor dollars into the energy sector (almost all of which is oil and gas) should have outsized effects. This comes after years of energy’s underperformance and shrinking percentage of the overall stock market. The S&P 500’s energy sector is worth about $2.3 trillion, which is only equal to the value of just Amazon. With the value the S&P 500’s most valuable company, Nvidia, you could almost buy the entire energy sector and Amazon.

- Aluminum, fertilizer, and other energy-intensive commodities have increasingly come from the Arabian Peninsula. Prices have started rising across the board. Fertilizer is attractive to us. Years of low prices and sentiment may have found their catalyst. Fertilizer stocks’ cheap prices provide a margin of safety.

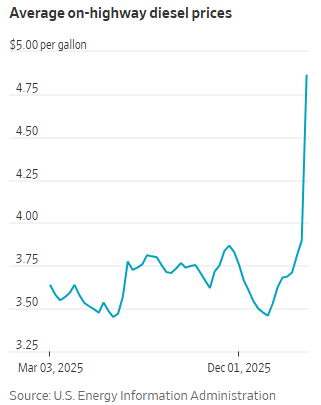

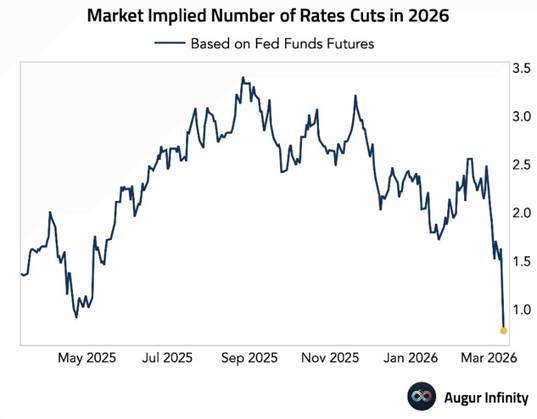

- Near-term inflation expectations have risen, which only strengthens the case for inflation protected Treasurys. The Federal Reserve’s job has become only harder. Estimates for rate cuts have declined as recent inflation figures have ticked up. Gasoline, diesel, and jet fuel prices have spiked. The Fed’s favorite inflation measure suggests the Fed’s target of 2% might not be obtainable in the near term.

- Economic growth data and expectations have started to sour. On Friday, GDP growth of Q4 2025 was revised downward, from a 1.4% annual rate to 0.7%. Meanwhile betting odds for a recession this year have risen. Combined with inflation news, markets may become less complacent about a monster not seen in nearly 50 years: stagflation.

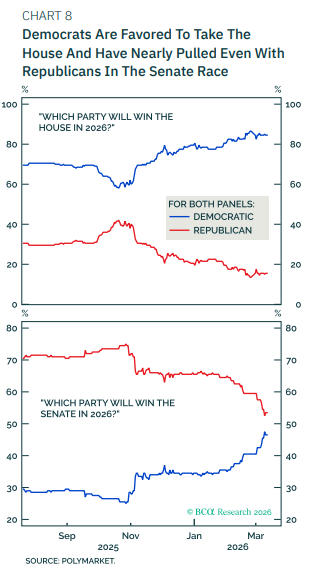

- The war has already had political implications. The odds of a Democratic sweep this November have increased, as has the odds of a Trump impeachment by 2028 (70% chance per Kalshi).

Source: BCA Research 3/12/2026

About the Author

Neil Rose, CFA, is the founder and CEO of Regency Capital Management.