China’s Real AI Advantage Isn’t the Algorithm—It’s the Electric Bill

We know AI is changing everything, but perhaps the bigger AI risks in the near term lie in AI’s geopolitical ramifications.

There’s already an arms race between the U.S. and China. The stakes are high, and the race is already closer than anyone thought.

The U.S. has long had an innovation edge, but China might have an equalizer: cheap power. Could China’s AI be accepted someday as a much better value?

Chinese platforms are improving by the day, and to many, the difference between theirs and the U.S.’s Claude, ChatGPT, Gemini, and others is negligible for many applications. China’s Moonshot released Kimi K2.6 in April, and it quickly became the second most used model on OpenRouter, the world’s largest AI routing platform, behind only Claude. In April 2026, eight of the top ten open-weight AI models came from Chinese labs.

Kimi and other leading Chinese platforms like DeepSeek and Alibaba’s Qwen are almost all open-source and open-weight, allowing developers to download, modify, and run them on local machines instead of Chinese servers.

But their biggest advantage is price. AI models generally come free of charge with only the most advanced versions of some requiring a fee that’s still significantly cheaper than U.S. competitors.

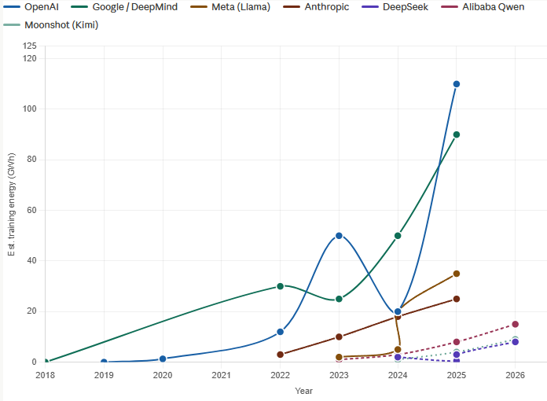

The cost advantage could widen over time as new AI releases require disproportionately more energy consumption. (At least this has been the trend thus far.)

Here’s the estimated training energy required over time as models improved:

Chinese companies represent a fundamental disruption to the economics of AI adoption. This is mostly because of China’s advantages in electrical infrastructure and cheaper power.

China has spent decades building out power capacity, including low-cost solar, wind, nuclear, and hydroelectric. Today, China’s power generation and transmission infrastructure delivers electricity at half the cost of that in the U.S.—a country that still lacks anything close to a national grid.

Meanwhile, even with major infrastructure spend in the U.S., including hundreds of billions of dollars annually from a handful of “hyperscalers” like Amazon and Google, demand growth should exceed supply growth for the foreseeable future. That means it’s likely power prices in the U.S. will continue to increase.

I think it’s probable the future of AI leadership will be shaped by power more than anything else. The winners might be those offering 95% or 98% the capability of the best or smartest AI model at any given time, but at a fraction of the cost. Like with medicine, wine, and textiles, in most product categories, the bulk of the price premium lives in the newest, most refined iteration. Premium is often defined by a thin layer of differentiation.

Most of the time, that outsized premium persists because of human biology and psychology. Fashion wouldn’t be so prominent otherwise.

But for crunching numbers, getting insights, and just getting things done, good enough is great if the price is right.

These are just observations and thinking about what’s next. This is not an endorsement of Chinese AI. We haven’t used any yet and will likely not for quite some time. Even then, any exploration into anything at the intersection of data and China would be done clinically, with local “air-gapped” machines disconnected from sensitive data.

The approach would look like that of scientists working in a lab with live pathogens.

For now, our hands are full with U.S.-based platforms. There is still so much to learn and do with AI.

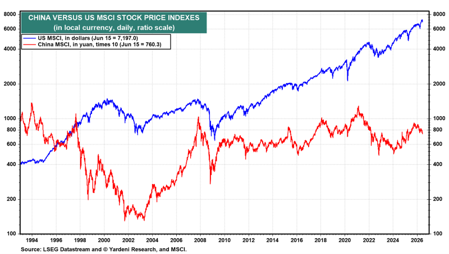

Lastly, a side note: anytime I think of China, I can’t help but look at the proverbial score board. There’s a striking economics lesson in the gap between China’s extraordinary economic and technological growth and its stock market prices.

The chart below shows some 30-plus years of U.S. and Chinese stock prices. For all the growth and progress of China (red line), there has been approximately zero profit on average in Chinese stocks while U.S. stocks (blue line) went up over 17-fold.

Economic growth itself is not enough. Rule of law, property rights, and economic mobility are needed for shareholders/owners to get returns for the capital risks they take.

About the Author

Neil Rose, CFA, is the founder and CEO of Regency Capital Management.