Two Americas: The Growing Tax Divide Between States

By Neil Rose, CFA

Federal tax law isn’t the whole story. Your taxes are increasingly determined by where you live.

There is a quiet revolution happening in American tax policy, and it has nothing to do with Washington. It’s happening in state capitals—and the divide is widening.

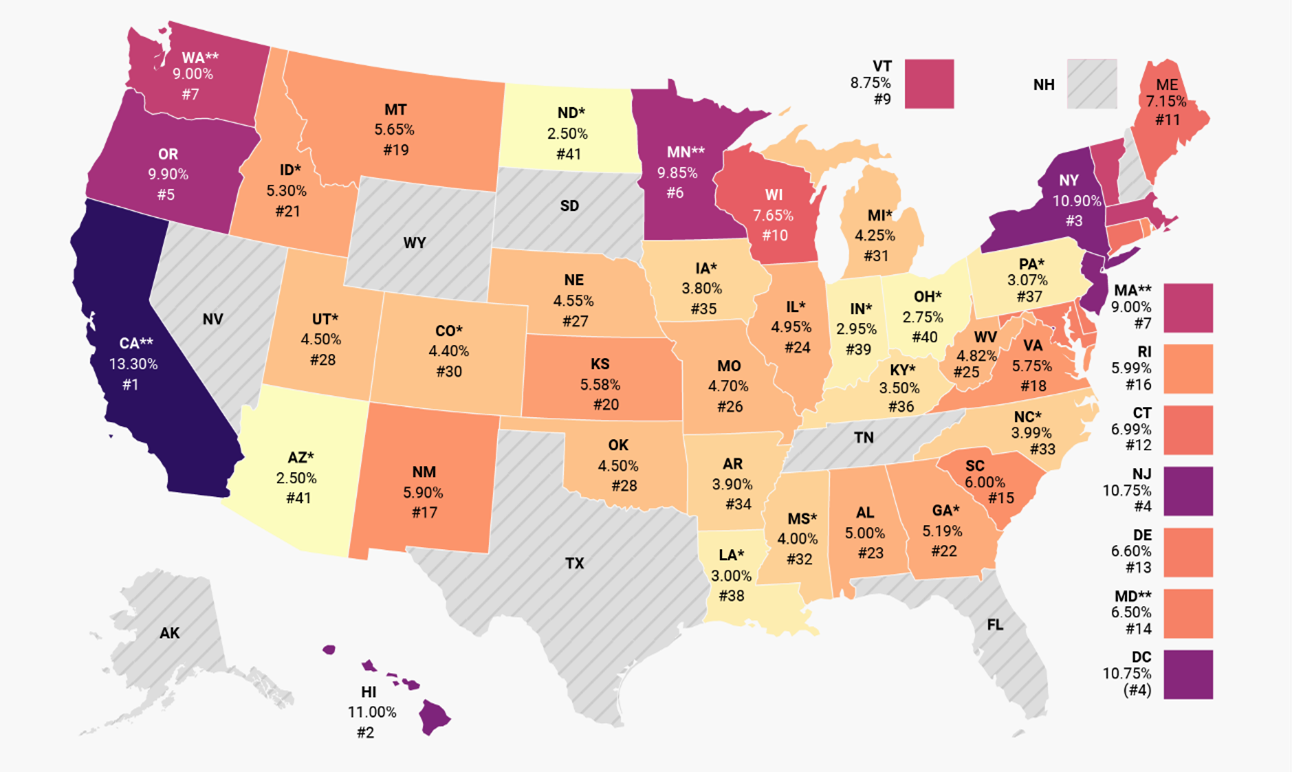

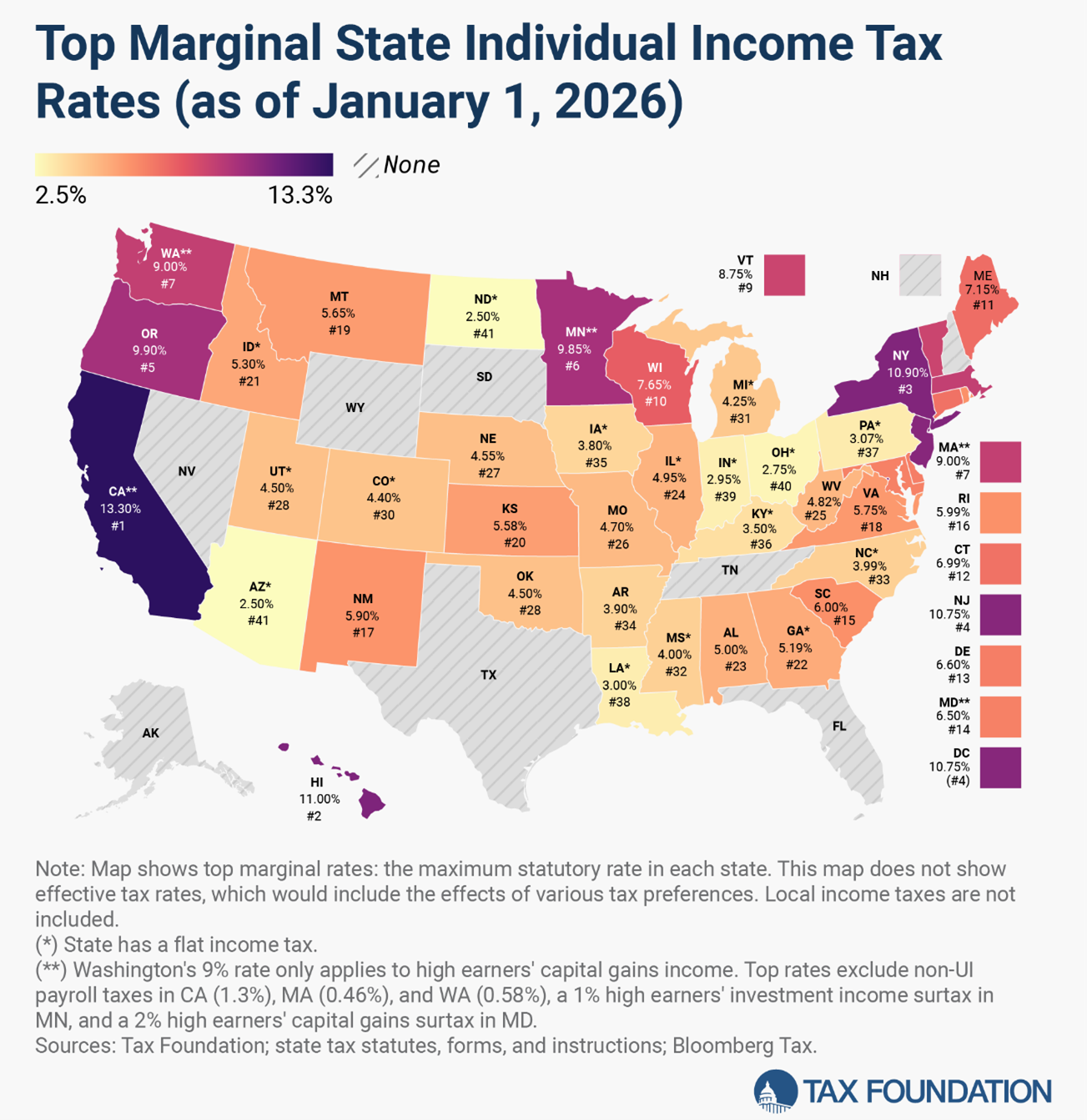

On one side: states like Texas, Florida, Nevada, Washington, Wyoming, South Dakota, and Tennessee, which have no individual income tax. On the other: California (up to 13.3%), Hawaii (up to 11%), New York (up to 10.9%), New Jersey (up to 10.75%), and Minnesota (up to 9.85%), all of which have continued to push rates higher, particularly on high earners.

Source: taxfoundation.org

The Math Is Getting Harder to Ignore

Consider a married couple with $1 million in taxable income. At the federal level, both face the same rates. But layer in state income taxes, and the difference is stark. That same couple pays roughly $137,000 more in income tax in California than they would in Florida or Texas. Over 20 years, assuming the money were invested, that gap compounds greatly.

OBBBA’s increase in the SALT deduction to $40,000 helps—but only modestly for high earners whose state and local tax bills can easily run $100,000 or more.

The Blue State Response

Rather than lowering rates to compete, several high-tax states are doubling down. California has been flirting with a state-level wealth tax for years. New York has proposed exit taxes designed to follow departing residents. More cities and counties now levy income tax. New York City’s highest income tax rate is 3.876%, which kicks in on income over $50,000. Some cities levy payroll taxes as well. New York City’s highest rate is 0.6%. Seattle charges employers a payroll tax of up to 2.4% and recently enacted a “Social Housing” payroll tax of 5% for high earners.

New state and local taxes are surely to come. In 2023, Washington enacted the nation’s first payroll tax for public long-term care. Today, a dozen states are considering doing the same. The overall direction of state and local taxation in many states is unmistakably up.

Residency Planning Is Now a Thing

For clients considering a move, retirement location, or second home strategy, the tax implications deserve a prominent seat at the planning table. True domicile change requires more than buying a condo in Florida. States like California and New York are aggressive auditors of residency claims. They want to see the full picture: where you spend your days, where your doctors are, where your clubs are, where your kids and even pets live.

The general rule of thumb—spending fewer than 183 days in a high-tax state—is a starting point, not a finish line. A well-documented move, executed properly, is entirely defensible. A casual, half-executed one invites scrutiny.

The Estate Tax Wrinkle

Federal estate taxes get a lot of attention, but state estate and inheritance taxes can surprise even sophisticated people. A dozen states (and D.C.) impose their own taxes—some with exemptions as low as $1 million. Hawaii, Oregon, and Washington have estate taxes that kick in well below the federal threshold. And the rates can be steep. Hawaii’s highest estate tax rate is 20%. Washington’s top rate is now 35%.

Maximize Happiness

Contrary to many approaches to financial planning, the goal of having a financial strategy—including planning for taxes and residency—should be to maximize happiness, not necessarily money. It is not uncommon for people to make significant changes and moves in their life based on taxes, only to be less happy and even miserable. Tax rates and financial efficiency are important, no doubt, but should be approached rationally, hard as that can be given taxes affect many of us on a visceral level.

There are many powerful and emotional factors at work when it comes to where to live, where to earn, and (increasingly) where to die. Taxes might be one of the easier considerations if you think about it. Taxes represent a price to occupy, earn, spend, and yes, die. They are not the only price, but they matter. The thing is, taxes matter more the more they cost.

The fiscal and macroeconomic effects will be revealed in time. For now, some states’ price increases are making more of their largest taxpayers (who are also their most mobile) decide to live elsewhere. States might learn there’s something worse than not having rich people pay more: not having enough rich people.

This material is for informational purposes only and does not constitute tax or legal advice. Please consult your tax professional for guidance specific to your situation.

About the Author

Neil Rose, CFA, is the founder and CEO of Regency Capital Management.